Characterization of Retirement Plans Overview

How are Retirement Plans Characterized in a Divorce?

California family law courts generally allocate retirement plan benefits between separate property and community property according to when the benefits were earned. Benefits “earned” during the marriage (after the date of marriage and before the date of separation) are generally characterized as community property. Benefits “earned” before the date of marriage or after the date of separation are generally characterized as separate property.

See our Practice Area Page on Retirement Plans

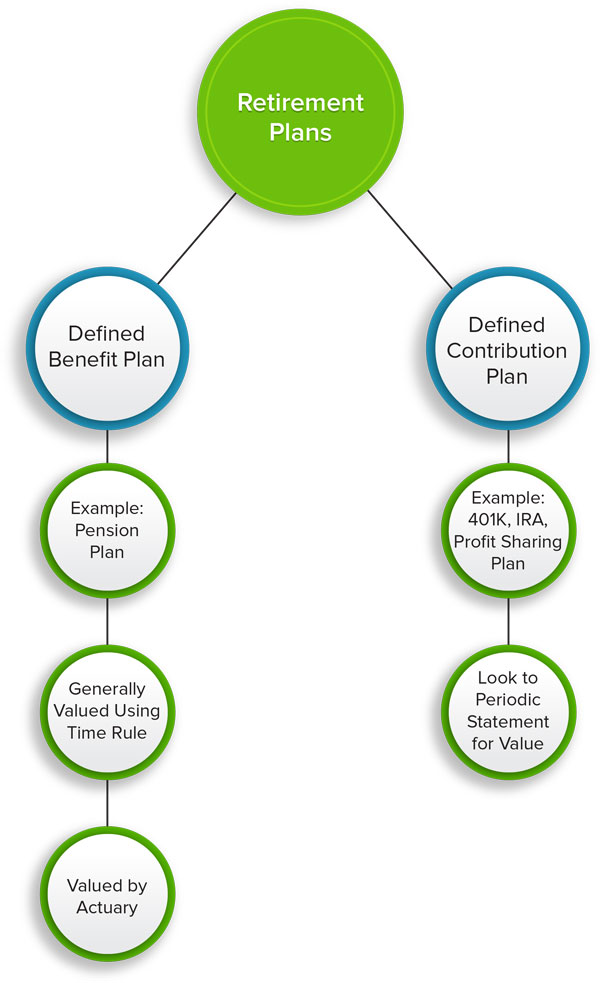

Two Basic Types Of Retirement Plans