Characterization of Deferred Compensation Allocation of Stock Options

Stock options, restricted stock, stock appreciation rights (SARs), phantom stock and restricted stock units (RSUs) may be granted to employees as a part of a compensation package. Generally, these types of assets have a risk of forfeiture.

Allocation Of Stock Options

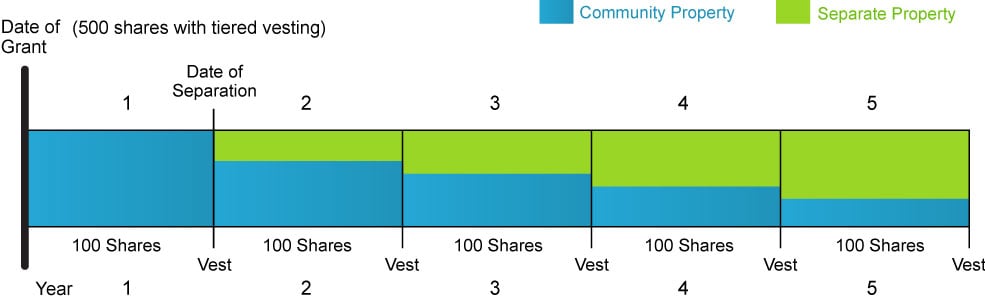

Stock options granted during the marriage and/or partially vested during the marriage may have a community property component. Stock options that are partially earned during the marriage are allocated between community property and separate property. The foundation for this allocation is the statutory law that provides that “earnings” during the marriage are community property. If a spouse is compensated during the marriage, in part, with a grant of stock options that partially vest during the marriage and partially vest after the date of separation, the stock options will most likely be partially community property. If a spouse’s employment during the marriage results in the partial vesting of stock options granted before the date of the marriage, the options will also most likely have a community property component. The number of options characterized as separate property or community property will vary depending upon which formula is used by the family law court.

The time rule is used to allocate options between community property and separate property. The time rule does not determine characterization. The characterization of an asset is determined by when the right to the asset was accrued.

Cliff Vesting

There are three basic formulas (IRMO Nelson, IRMO Hug and IRMO Harrison) used to allocate options between separate property and community property. Generally, the community’s percentage interest in stock options that vest after the date of separation decreases as each year lapses.

Divorce courts look to a number of factors in determining which formula to use:

- When was the grant made?

- Were the stock options granted to attract and retain the employee?

- Were the stock options granted for past service?

- Were the stock options granted to offset under-compensation?

- What are the forfeiture provisions?

- What are the vesting dates?

- What are the vesting provisions?

- Are the stock options designed as “golden handshakes” to retain the employee?

- What was the strike price at the time of grant?

- When did the parties separate?

- When did the parties marry?

- Were the stock options granted to replace other stock options?